There are several different types of IRA-based retirement plans available to individuals and to employers. Each has different qualifications, contribution limits, tax-filing requirements, and distributions. This article will define each and illustrate their benefits.

Traditional and Roth IRAs

Traditional and Roth IRAs are available to anyone with earned income, regardless if you are a participant in another retirement plan sponsored by your employer or business. These are established by the employee with financial institutions. Here are the details of how they work:

- $5,500 contribution limit ($6,500 for taxpayers over the age of 50 at the end of the calendar year)

- Traditional IRA: Contributions made are either fully or partially deductible, depending on taxpayer AGI. Earnings on the account balance are not taxed until they are distributed.

- Roth IRA: Contributions made to the plan are not tax-deductible and qualified distributions are tax-free

- Employees can contribute to a Roth IRA after 70 ½ years old, but cannot after that time for a traditional IRA.

Employer IRA-Based Retirement Plans

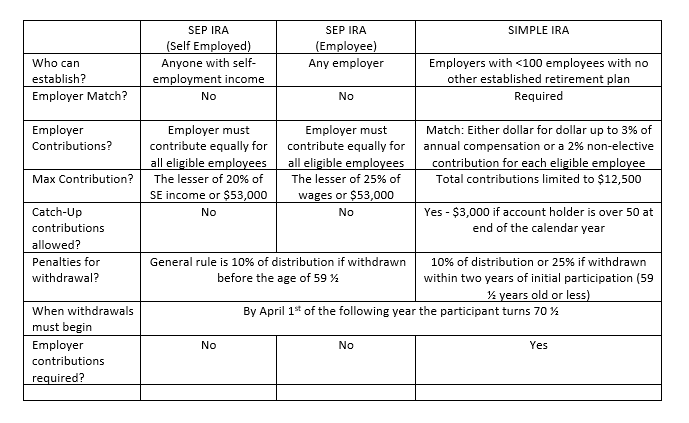

The following are IRA-based plans available to employers. I have also offered a comparison table summarizing the important points at the end in order to help you make your decision about which plan to offer to your employees.

Simplified Employee Pension Plan (SEP)

The SEP allows employers to contribute to both employees and their own retirement plans. Businesses of any size may establish one and there is no tax filing requirement for the employer. With a SEP, the employer contributes to traditional IRAs set up for each employee. An employer must contribute equally for all eligible employees, and if a SEP fund is established, all eligible employees must be participants. Here are some details regarding contributions and withdrawals:

- Contributions are made by employers directly to individual IRAs set up for each employee, and invested in funds of their choosing.

- A contribution, not to exceed the lesser of 25 percent or $53,000 of an employee’s pay, may be deposited to the plan in a given year.

- Employee is always 100 percent vested in the IRA money.

- Annual contributions are flexible year to year.

- No salary deferrals or catch-up contributions are permitted (two things often synonymous with 401k plans).

- Participant loans are not permitted (assets may not be used as collateral).

- In-service withdrawals are allowed and will be treated as ordinary income and subject to an additional 10 percent penalty tax if the participant is under 59 ½ years old.

Simple IRA Plan

This savings incentive match plan is available to, and best suited for, any small business with 100 or fewer employees. It allows employers and employees to contribute to traditional IRAs set up for employees. Here are the rules:

- The employer cannot have any other established retirement plan.

- Employer-required contributions include:

- Matching contribution dollar-for-dollar up to three percent of annual compensation, or

- A two percent non-elective contribution for each eligible employee.

- Employees may elect to contribute and are always 100% vested in all Simple IRA money.

- Total contributions are limited to $12,500 for 2015-2017. Participants over 50 at the end of the calendar year may make an additional $3,000 catch-up contribution, if permitted by the plan.

Employer Plan Comparison Table

As you can see, there are various options and choices to make based on your business and it employees. You can find more detail at the IRS website here: https://www.irs.gov/retirement-plans/ira-based-plans. As always, if you would like further information, please get in touch with your tax advisor.

---

The information contained in the Knowledge Center is intended solely to provide general guidance on matters of interest for the personal use of the reader, who accepts full responsibility for its use. In no event will CST or its partners, employees or agents, be liable to you or anyone else for any decision made or action taken in reliance on the information in this Knowledge Center or for any consequential, special or similar damages, even if advised of the possibility of such damages.